Digital identification is encouraged to address COVID-19 challenges

COVID-19 has thrown a number of challenges to the financial sector. We have seen a large spike in online application volumes across most industries, particularly stockbroking, highlighting the lack of scalability with non-digital client onboarding and identity verification processes.

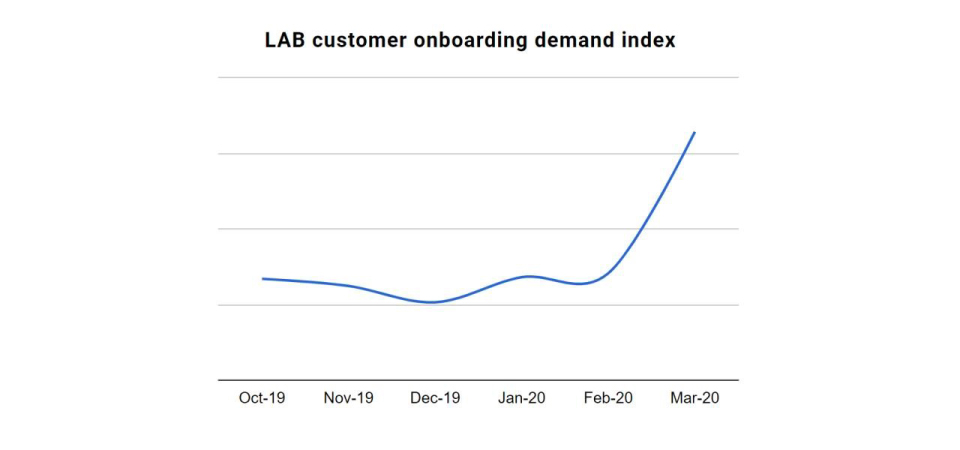

Google Trends revealed that searches for "how to buy stocks" surged in March. This was certainly evident in the LAB customer onboarding demand as significantly more people opened accounts online to invest in shares, managed funds and even gold.

With it becoming increasingly difficult for investors to get documents certified and sent in, a large backlog of unfulfilled accounts is occurring across the industry. Those with digital and straight through processes are faring better than others at this time.

Financial Action Task Force (FATF) encourages digital onboarding

The Financial Action Task Force (FATF) is strongly encouraging digital customer onboarding and financial services delivery.

The FATF has noted that with people confined or facing social distancing measures, accessing financial services in-person is difficult, and creates unnecessary exposure to infection. Financial technology provides significant opportunities to manage some of the wider issues associated with COVID-19.

In line with the FATF Standards, the FATF encourages the use of technology, including Fintech, Regtech and Suptech to the fullest extent possible. The FATF’s Guidance on Digital ID, highlights the benefits of trustworthy digital identity for improving the security, privacy and convenience of identifying people remotely while also mitigating ML/TF risks.

More on the FATF statement here

For more information, please contact your Customer Success Manager.

AUSTRAC releases KYC guidance

AUSTRAC has released guidance on complying with KYC requirements during the pandemic. It recognises that some KYC processes cannot be used at this time and has outlined the following alternative ways to verify customers identity and fulfil KYC requirements:

- using alternative proof of identity processes (Rule 4.15.1)

- using electronic copies (scans or photographs) of reliable and independent documentation, to verify the identity of individual customers (Rule 4.9.3(3)) or companies (Rule 4.9.5(3))

- relying on disclosure certificates to verify certain types of information about customers who are not individuals (Rules 4.3.12, 4.4.16, 4.5.8, 4.6.8 and 4.7.8)

Once customers have provided copies of identification documents, AUSTRAC advises organisations to consider additional verification through:

- a video call to compare the physical identity of the customer with scanned or photographed copies of identification documents

- requiring a customer to provide a clear, front-view ‘selfie’ of themselves that can be compared with the scanned or photographed copies of identification documents

- telephoning the customer to ask questions about their identification, their reason for requesting a designated service or other questions that would assist in ascertaining whether the customer is who they claim to be.

More on AUSTRAC’s guidance here.

LAB is working with strategic partners to deliver facial biometrics technology to enable verification of identification anywhere, anytime.

New AUSTRAC rule supports the early release of superannuation

In response to the impacts of Covid-19, the Federal Government is allowing a temporary early release of superannuation. Superannuation fund members who meet eligibility criteria can withdraw $20,000 of their superannuation tax free - $10,000 before 1 July and $10,000 between 1 July and 24 September 2020.

To streamline the process for making these payments, AUSTRAC will introduce a new rule under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF). This enables funds to make payments without having to conduct additional customer verification if the payment has been approved by the ATO.

More on the AUSTRAC rule here.

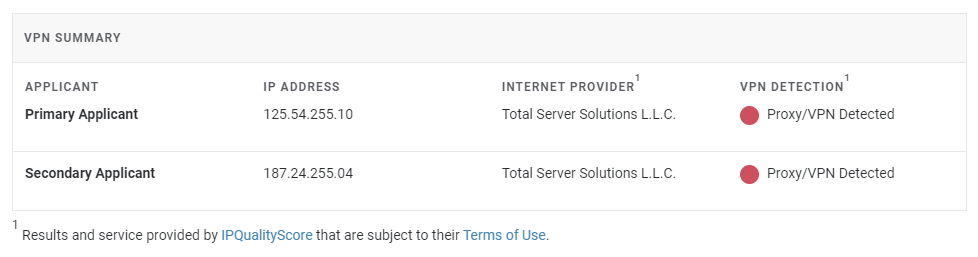

Our VPN detection solution is now active

Identity theft and the use of stolen information to create fraudulent accounts is a significant and costly issue. Virtual Private Networks (VPNs) are a common tool used by fraudsters to mask their internet activity and identity.

We recently released a new VPN detection solution to help identify potential fraudulent applications. This is now active in your LAB Application Manager. Go to the application details view of any new application, and you’ll see it displayed in the VPN Summary table.

If VPN detection results are available and a VPN is detected, you can take action to confirm the application is authentic prior to proceeding with your usual account opening processes.

For more information on how to activate this feature, please contact your Customer Success Manager.

Open banking and CDR moving forward

The ACCC has formally set the rules for the Consumer Data Right (CDR). These detail how the scheme works and what the banks are legally required to do. Open banking is due to launch on 1 July 2020.

We understand that many Australian businesses are still developing their information systems to meet the CDR requirements in order to share data in real time.

The CDR privacy guidelines explain how businesses must protect consumer data. We at LAB have been actively following and contributing to how the CDR regime may apply to third party providers, see our submission to the ACCC here.

New requirements for advisers under FASEA

The Financial Adviser Standards and Ethics Authority (FASEA) Code of Ethics came into effect on 1 January this year. It includes a range of requirements for advisers providing personal financial advice and services to retail clients. It does not apply for sophisticated investors and other wholesale clients.

There may be greater scrutiny on how advisers determine who is a sophisticated investor. Clients who meet the wealth test (at least $2.5 million in net tangible assets and over $250,000 in annual income) must also have the investment experience and knowledge to qualify, or else be treated as a retail client.

It is up to the adviser to assess whether a client is financially competent. Failure to do this could lead to a breach of the Code’s standards and the Corporations Act.

AFSL holders must be able to prove that they are complying with the code and that they have processes in place to meet all the retail obligations.

We expect that in time FASEA will provide further guidance, but given the extremely broad interpretation of the Code, advisers should be cautious.

LAB client Suitability Questionnaires

LABform Questionnaires are designed to digitally collect information from applicants/investors to facilitate additional screening or profiling to ensure they are suitable for a given product.

Common uses for questionnaires are:

- Risk profiling

- Capturing investment objectives

- Suitability screening

- Pre-product screening

- Capturing general information

- Determination of sophisticated investor status

The following features and options are supported by LABform:

- Pooled questions

- Weighted questions

- Calculated results (Overall score or pass/fail)

- Locked results

- product screening